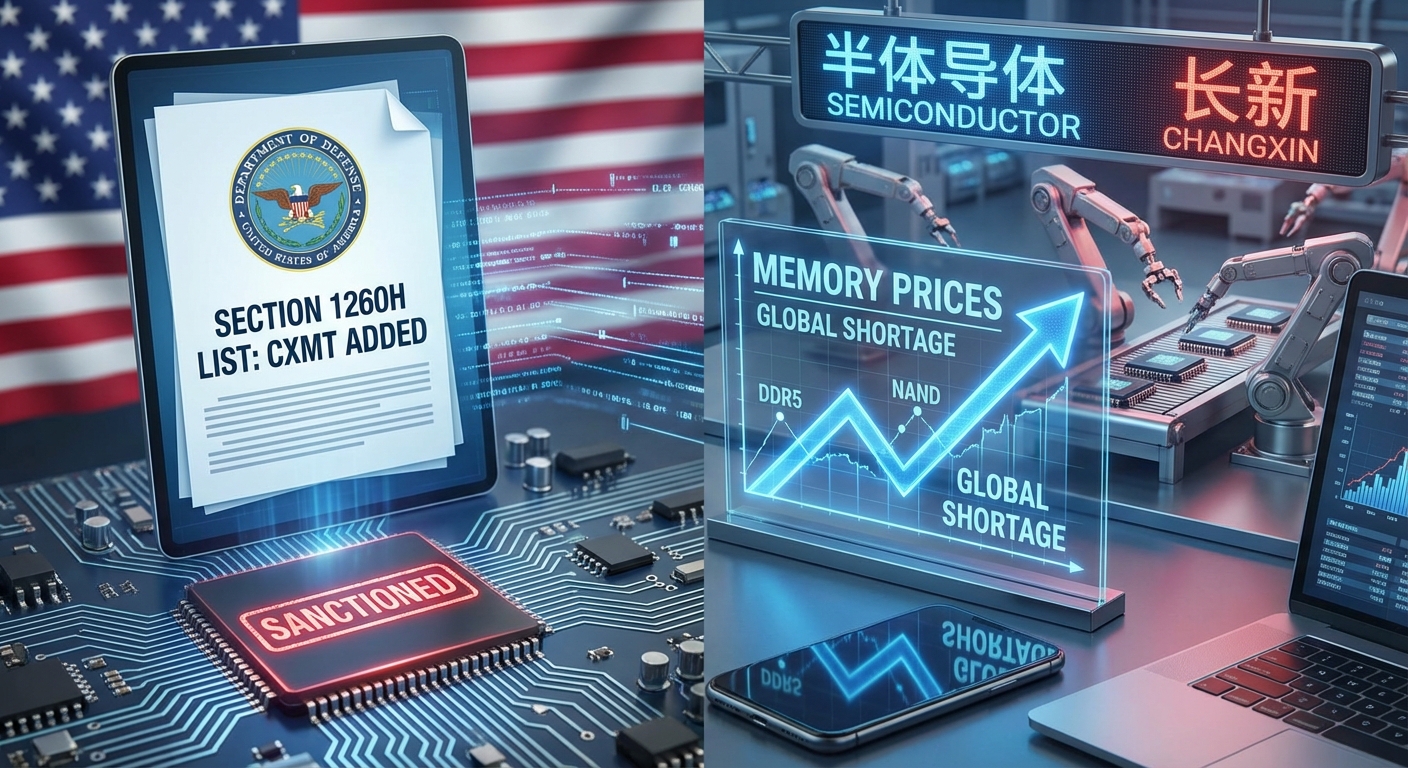

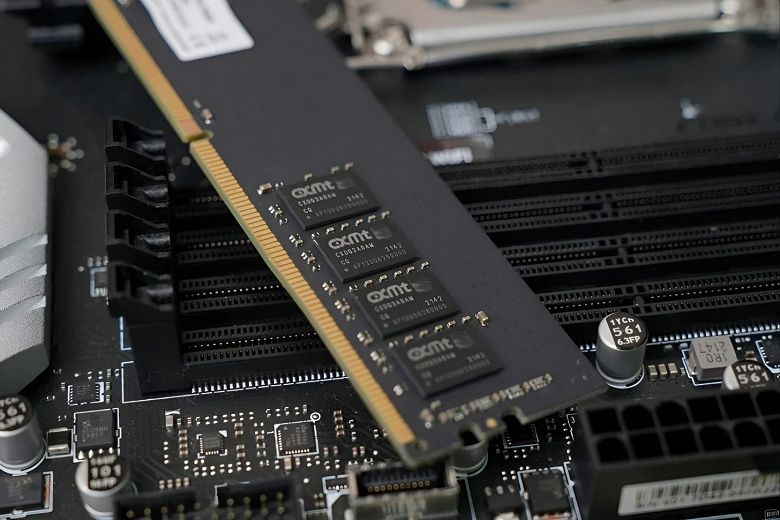

In a move that complicates the global semiconductor supply chain, the Pentagon has officially added China’s leading DRAM manufacturer, ChangXin Memory Technologies (CXMT), to its list of alleged “Chinese military companies.” This development contradicts earlier speculation about a potential easing of restrictions and places CXMT alongside NAND producer Yangtze Memory Technologies Corp (YMTC), which is already under stricter U.S. sanctions. While this appears to close the door on Chinese memory for Western device makers, a severe global memory shortage and skyrocketing prices are creating powerful counter-pressures that could reshape the industry.

A Tale of Two Blacklists

It’s crucial to understand the different U.S. government lists targeting Chinese tech firms. CXMT was added to the Pentagon’s Section 1260H list in January 2025. This designation does not impose immediate trade bans but serves as a strong warning to U.S. companies about the risks of collaboration and will prohibit the Department of Defense from procuring products from these firms starting in June 2026. The initial news about a potential delisting, which arose from a quickly retracted document, created temporary confusion but was ultimately proven false by the official addition.

YMTC, on the other hand, has been on the much more restrictive Commerce Department’s Entity List since late 2022. This listing severely limits its access to U.S. technology and makes it very difficult for American companies and their partners to supply or do business with them.

The Market’s Invisible Hand: Shortages and Price Hikes

The backdrop to these geopolitical maneuvers is a turbulent market. The world’s top three memory makers-Samsung, SK Hynix, and Micron-are increasingly dedicating production capacity to high-margin, high-bandwidth memory (HBM) to meet the voracious demands of the AI industry. This strategic shift has created a significant supply gap for conventional DRAM and NAND flash memory used in PCs, smartphones, and other consumer electronics.

The consequences are stark: memory prices are entering a “super cycle” of sharp increases. Some reports from early 2026 noted that prices for certain DDR5 memory kits had surged nearly fivefold in just a few months. TrendForce analysts predicted that conventional DRAM contract prices could jump by 55-60% in the first quarter of 2026 alone. This extreme price pressure is forcing major PC manufacturers like HP, Dell, Acer, and Asus to explore all available options to manage costs.

A Look to the Future

The U.S. government’s actions send a clear signal of its intent to decouple critical technology supply chains from China. However, market forces are pushing in the opposite direction. The soaring cost of memory from traditional suppliers creates a powerful incentive for OEMs to consider alternatives, even if they come with political and compliance risks. While Chinese DRAM makers are reportedly selling legacy chips at half the price of major competitors, the long-term reliability and quality for high-end Western products remain a question for large-scale adoption.

The coming years will reveal which force is stronger: geopolitical policy or market reality. The decision by major manufacturers on whether to absorb higher costs or navigate the complex landscape of sanctions to work with companies like CXMT will have long-lasting consequences for the global technology ecosystem.