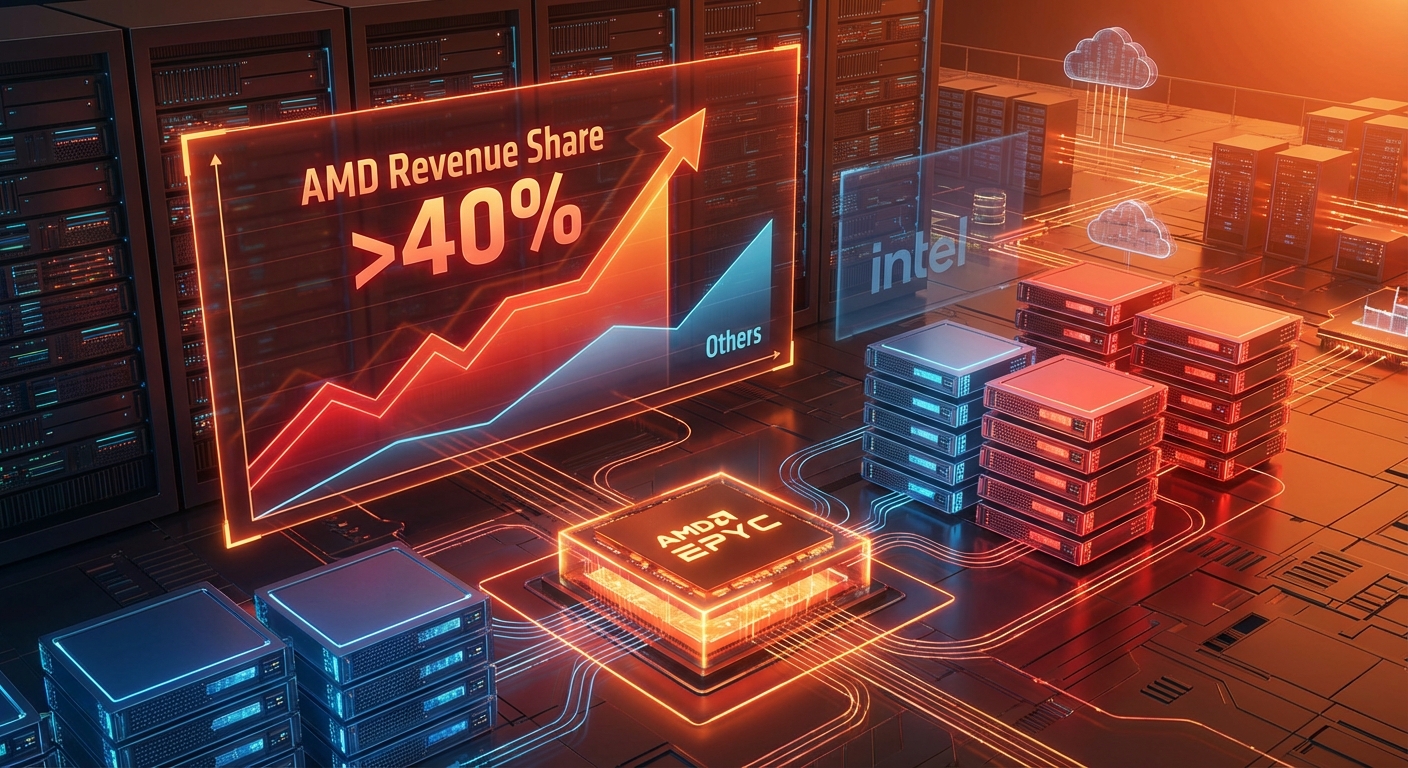

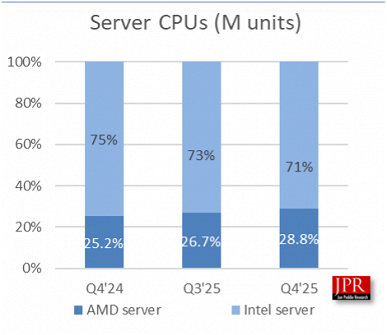

Recent data from analyst firm Jon Peddie Research (JPR) confirms a significant power shift in the server CPU market, with AMD continuing its relentless advance at the expense of its rival, Intel. According to the latest Q4 2025 reports, which align perfectly with findings from Mercury Research, AMD’s unit share in the server segment has climbed to a record 28.8%. This marks a steady increase from 26.7% in the previous quarter and 25.2% just one year prior. However, the unit shipment figures only tell part of the story; a deeper look at revenue reveals an even more dramatic trend. For the first time, AMD’s server CPU revenue share has surpassed the 40% threshold, reaching an all-time high of 41.3%.

The Story in Numbers: Quality Over Quantity

The disparity between unit share (28.8%) and revenue share (41.3%) is crucial. It indicates that AMD is not just selling more server processors, but it is increasingly selling higher-value, premium EPYC chips that command a higher average selling price (ASP). In contrast, Intel now holds 71.2% of the unit share but captures only 58.7% of the revenue, suggesting a reliance on lower-priced models to maintain volume. This success is attributed largely to the strong adoption of AMD’s 5th generation EPYC processors, codenamed “Turin,” which for the first time accounted for more than half of the company’s server revenue. Meanwhile, Intel’s 5th Gen Xeon “Emerald Rapids” chips have become its best-selling server line.

This trend isn’t isolated to the data center. AMD has seen explosive growth across all segments. In the desktop PC market, its unit share climbed to a record 36.4%, while its revenue share hit an even more impressive 42.6%, fueled by the popular Ryzen series. Even in the mobile segment, traditionally an Intel stronghold, AMD reached a new high of 26% unit share.

Behind the Surge: A Perfect Storm of Opportunity

Several factors have contributed to AMD’s accelerated growth. A key element was Intel’s own strategic decisions. Faced with high demand and manufacturing constraints, Intel prioritized the production of its high-margin server CPUs. This move, however, led to supply shortages in its desktop and mobile client segments, creating a significant opening that AMD capitalized on with its competitive product stack. Furthermore, the unprecedented boom in AI and high-performance computing (HPC) has massively increased demand for data center processors. While both companies benefited, AMD’s server shipments grew at what Mercury Research described as “more than triple the average” seasonal rate, outpacing Intel’s growth.

A Look at the Broader Market

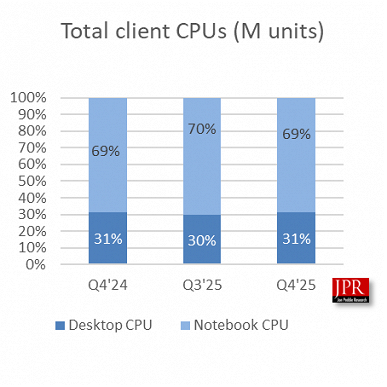

JPR’s analysis also sheds light on the overall PC market composition. The ratio of mobile to desktop CPU shipments remains stable year-over-year at 69% and 31%, respectively. This confirms that the demand for laptops continues to be more than double that of desktop PCs, highlighting the strategic importance of AMD’s recent gains in the mobile sector.

The Road Ahead: An Intensifying Battle

Looking forward, the server CPU market is projected to continue its rapid expansion, with some analysts predicting it could become a $60 billion industry by 2030. AMD is positioning itself to capture an even larger piece of this growing pie, with some company estimates suggesting a long-term goal of securing more than half of the market. However, Intel is actively working to counter this momentum. The company is investing heavily in regaining process technology leadership with its upcoming 18A node and is preparing to launch new product families like Panther Lake and Nova Lake to challenge AMD across all fronts. The competitive landscape is further complicated by the rise of ARM-based alternatives from companies like Nvidia and custom silicon solutions from major cloud providers. While AMD’s current trajectory is formidable, the battle for data center dominance is set to intensify in 2026.